What are scope 1 2 and 3 emissions: A Complete Guide

.jpeg)

Scope 1, Scope 2 & Scope 3 Emissions Explained (With Examples)

As climate regulations tighten and ESG disclosures become mandatory, businesses are under growing pressure to understand where their emissions come from and how they are measured. Most sustainability strategies fail not because of lack of intent, but because companies don’t have a clear, structured view of their emissions footprint.

This is where Scope 1, Scope 2, and Scope 3 emissions come in.

Defined by the Greenhouse Gas (GHG) Protocol, these three categories help organizations identify direct emissions, energy-related emissions, and value-chain emissions—creating a complete picture of climate impact and accountability.

In this guide, we break down what Scope 1, 2, and 3 emissions are, how they differ, and why Scope 3 has become the biggest challenge in ESG reporting today.

Scope 1, Scope 2, and Scope 3 Emissions — Quick Definition

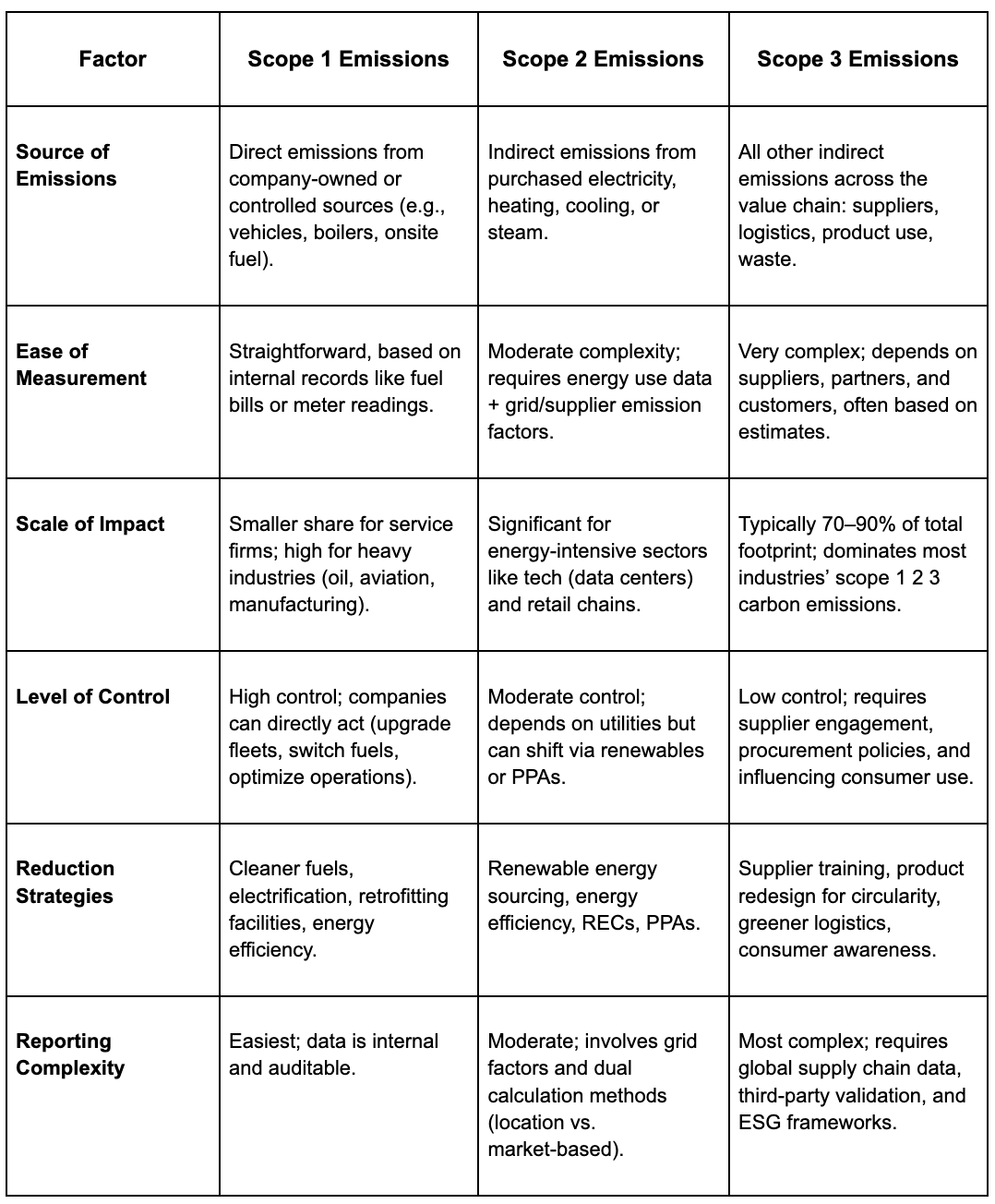

- Scope 1 emissions are direct emissions from sources a company owns or controls, such as fuel burned in company vehicles or onsite equipment.

- Scope 2 emissions are indirect emissions from purchased energy, including electricity, heating, or cooling consumed by the business.

- Scope 3 emissions include all other indirect emissions across the value chain, such as suppliers, transportation, product use, and waste. For most companies, Scope 3 represents the largest share of total emissions.

What Are Scope 1 Emissions? (Direct Emissions)

Scope 1 emissions come from sources that are owned or directly controlled by the company. These emissions are generated on-site or through assets the business operates.

Common Scope 1 Emissions Examples

- Fuel combustion in company-owned vehicles

- Onsite boilers, furnaces, and generators

- Emissions from manufacturing processes

- Refrigerant leaks from cooling systems

Because companies have direct control over these sources, Scope 1 emissions are usually the easiest to measure and reduce.

What Are Scope 2 Emissions? (Purchased Energy Emissions)

Scope 2 emissions are indirect emissions created during the generation of energy that a company purchases and consumes.

Even though these emissions occur at a utility provider’s facility, they are counted as part of the company’s footprint because the energy is used for business operations.

Common Scope 2 Emissions Examples

- Electricity used in offices, plants, or data centres

- Purchased heating, steam, or cooling

- District energy consumption

Scope 2 emissions highlight how energy sourcing decisions—such as switching to renewables—directly affect a company’s climate impact.

What Are Scope 3 Emissions? (Value Chain Emissions)

Scope 3 emissions cover all other indirect emissions that occur across a company’s upstream and downstream value chain. This includes emissions from activities the company does not own or directly control.

For most organizations, Scope 3 accounts for 70–90% of total emissions, making it the most material—and the hardest to measure.

Scope 3 Emissions Examples

- Purchased goods and services

- Supplier manufacturing emissions

- Transportation and logistics

- Business travel and employee commuting

- Product use and end-of-life disposal

- Investments and financed emissions

Because Scope 3 depends on third-party data, it requires supplier engagement, estimation models, and advanced data systems to track accurately.

Scope 1 vs Scope 2 vs Scope 3: Key Differences

1. Source of Emissions

- Scope 1: Direct, company-controlled sources

- Scope 2: Indirect emissions from purchased energy

- Scope 3: Indirect emissions across the entire value chain

2. Control and Accountability

- Scope 1 offers the highest level of control

- Scope 2 can be influenced through energy choices

- Scope 3 requires collaboration with suppliers and partners

3. Measurement Complexity

- Scope 1: Low complexity

- Scope 2: Moderate complexity

- Scope 3: High complexity due to external data dependency

4. Share of Total Emissions

- Scope 1: Usually the smallest share

- Scope 2: Moderate, energy-dependent

- Scope 3: Often the largest contributor

How to Measure Scope 1, 2, and 3 Emissions

Step 1: Define Reporting Boundaries

Identify which facilities, operations, and value-chain activities are included under each scope.

Step 2: Collect Activity Data

- Fuel usage

- Electricity consumption

- Supplier data

- Logistics and travel information

Step 3: Apply Emission Factors

Convert activity data into CO₂e using standardized emission factors aligned with the GHG Protocol.

Step 4: Consolidate and Analyze

Aggregate emissions across all scopes to identify hotspots and reduction opportunities.

Step 5: Report and Verify

Disclose emissions in line with frameworks such as CDP, GRI, TCFD, BRSR, or CSRD, ensuring transparency and audit readiness.

How to Reduce Scope 1, 2, and 3 Emissions

Reduce Scope 1 Emissions

- Electrify fleets and equipment

- Improve energy efficiency

- Switch to low-carbon fuels

Reduce Scope 2 Emissions

- Procure renewable electricity

- Enter power purchase agreements (PPAs)

- Invest in onsite renewable energy

Reduce Scope 3 Emissions

- Engage suppliers on emissions reporting

- Optimize logistics and transportation

- Redesign products for circularity

- Influence customer usage patterns

Turning Scope 1, 2 & 3 Data Into Action

Understanding Scope 1, Scope 2, and Scope 3 emissions is the foundation of any credible climate or ESG strategy. But manual spreadsheets and fragmented supplier data make accurate reporting difficult at scale.

This is where Breathe ESG helps businesses move from estimation to execution.

With AI-powered automation, Breathe ESG simplifies emissions data collection, ensures accurate Scope 3 tracking, and generates assurance-ready disclosures aligned with global frameworks. Companies can identify hotspots, set science-based targets, and demonstrate measurable progress toward net-zero goals.

Book a demo to see how streamlined Scope 1, 2 & 3 emissions tracking can support your ESG journey.

FAQs

What are the scope 1 and 2 emissions in the US?

In the US, scope 1 emissions come from direct company activities like fuel combustion in boilers, furnaces, and company vehicles. Scope 2 emissions are indirect, resulting from purchased electricity, heat, or steam. Both categories are central to corporate carbon accounting because they reflect energy choices and operational efficiency, forming the foundation for regulatory reporting and climate strategies.

What is the difference between scope 2 and 3?

Scope 2 emissions cover indirect greenhouse gases from purchased energy—electricity, heating, or cooling consumed by an organization. Scope 3 emissions, on the other hand, include all other indirect emissions in the value chain, such as supplier activities, transportation, product use, and disposal. The key difference is scale: scope 2 is limited to energy, while scope 3 extends across the entire supply chain.

How to calculate scope 1, 2, and 3 emissions?

Calculating emissions involves collecting activity data and applying standardized emission factors. Scope 1 uses direct fuel consumption data, scope 2 requires energy bills and regional grid emission factors, and scope 3 relies on supplier disclosures, logistics data, and life cycle assessments. Companies often use greenhouse gas protocols and carbon accounting software to standardize results, ensuring consistency, transparency, and assurance-ready reporting across all scopes.

Do all companies have scope 3 emissions?

Yes, nearly all companies generate scope 3 emissions because they account for upstream and downstream activities. Even service-based firms with minimal operations still rely on purchased goods, employee commuting, digital infrastructure, and waste management. For manufacturers and retailers, scope 3 can make up over 70% of their total footprint, making it the most complex but critical category to address for meaningful climate impact.